The South Korean market has skilled a slight downturn previously week with a 1.4% drop, but it maintains a constructive trajectory over the past yr, displaying a 4.3% enhance. On this context of anticipated earnings development and present market dynamics, dividend shares like Sebo Manufacturing Engineering & Building can supply traders potential stability and regular earnings streams.

High 10 Dividend Shares In South Korea

|

Title |

Dividend Yield |

Dividend Score |

|

Kia (KOSE:A000270) |

4.57% |

★★★★★★ |

|

Shinhan Monetary Group (KOSE:A055550) |

4.47% |

★★★★★☆ |

|

KT (KOSE:A030200) |

5.46% |

★★★★★☆ |

|

KB Monetary Group (KOSE:A105560) |

4.01% |

★★★★★☆ |

|

LOTTE High quality Chemical (KOSE:A004000) |

4.02% |

★★★★★☆ |

|

HANYANG ENGLtd (KOSDAQ:A045100) |

3.16% |

★★★★★☆ |

|

Snt DynamicsLtd (KOSE:A003570) |

3.95% |

★★★★☆☆ |

|

Korea Solid Iron Pipe Ind (KOSE:A000970) |

6.07% |

★★★★☆☆ |

|

Samyang (KOSE:A145990) |

3.38% |

★★★★☆☆ |

|

Hansae Yes24 Holdings (KOSE:A016450) |

5.27% |

★★★★☆☆ |

Click on right here to see the complete listing of 70 shares from our High KRX Dividend Shares screener.

We’ll study a range from our screener outcomes.

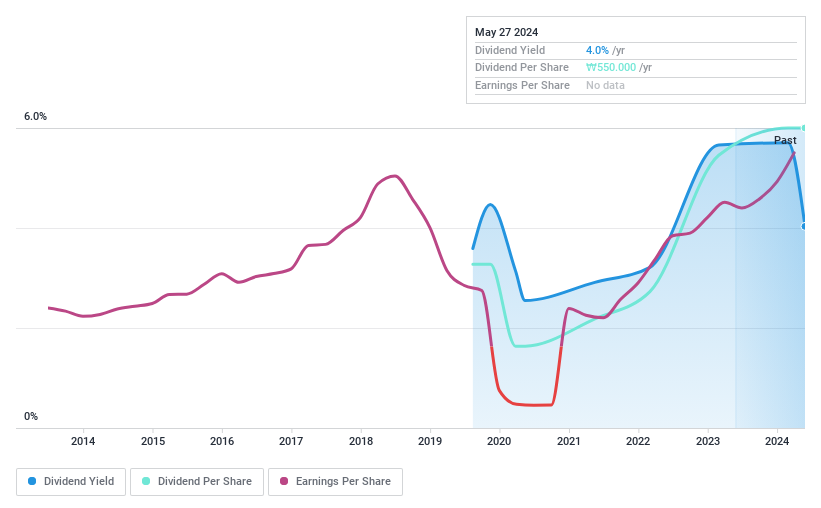

Merely Wall St Dividend Score: ★★★★☆☆

Overview: Sebo Manufacturing Engineering & Building Corp. operates within the building and engineering sector with a market capitalization of roughly ₩136.46 billion.

Operations: Sebo Manufacturing Engineering & Building Corp. doesn’t have detailed income phase info out there.

Dividend Yield: 4%

Sebo Manufacturing Engineering & Building has a robust protection of dividends by each earnings and money flows, with payout ratios of 15.5% and 5.5% respectively, indicating a stable monetary capability to take care of its dividend funds. Regardless of this, the dividend historical past is marked by volatility and unreliability over its brief 10-year distribution interval. The agency’s latest share repurchase program, valued at KRW 3 billion, goals to boost shareholder worth and stabilize the inventory value, reflecting proactive administration actions in favor of traders. Moreover, Sebo’s price-to-earnings ratio stands at a beautiful 3.9x in comparison with the broader Korean market common of 13x.

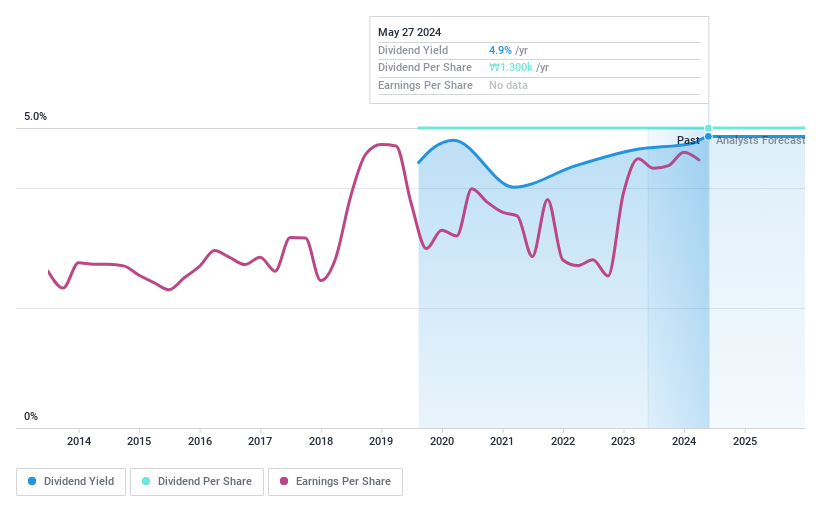

Merely Wall St Dividend Score: ★★★★☆☆

Overview: Geumhwa Plant Service & Building Co., Ltd. focuses on plant upkeep and building providers, with a market capitalization of roughly ₩157.98 billion.

Operations: Geumhwa Plant Service & Building Co., Ltd. doesn’t have detailed income phase info out there.

Dividend Yield: 4.9%

Geumhwa Plant Service & Building maintains a conservative dividend method with a payout ratio of 20.8% and a money payout ratio of 36.7%, making certain dividends are well-covered by each earnings and money flows. Regardless of its engaging dividend yield of 4.86%, which ranks within the high quartile of Korean dividend payers, the corporate’s dividend historical past is marred by instability, with no development over its five-year fee interval. Moreover, earnings are projected to say no yearly by 10.2% over the following three years, posing potential challenges for future dividend sustainability.

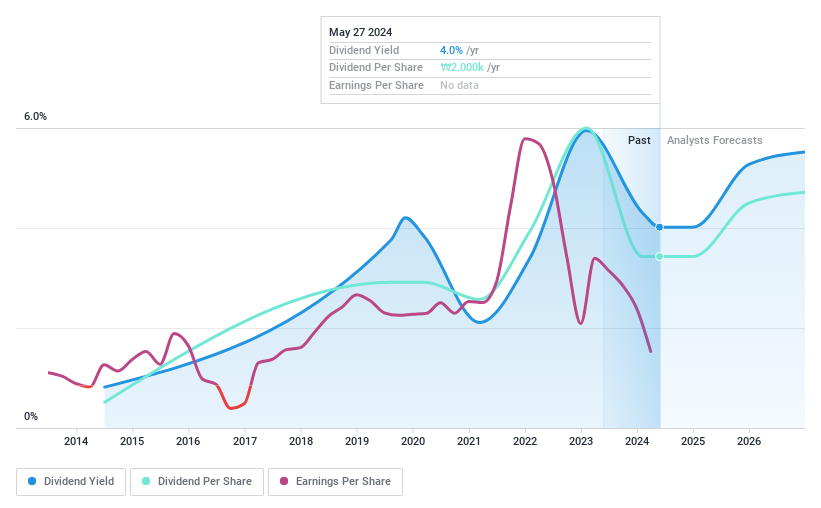

Merely Wall St Dividend Score: ★★★★★☆

Overview: LOTTE High quality Chemical Co., Ltd. specializes within the manufacturing and distribution of chemical merchandise in Korea, with a market capitalization of roughly ₩1.27 trillion.

Operations: LOTTE High quality Chemical Co., Ltd. generates its income primarily from the manufacturing and distribution of chemical merchandise in Korea.

Dividend Yield: 4%

LOTTE High quality Chemical has exhibited a combined efficiency with its dividends, marked by volatility over the previous decade. Regardless of this inconsistency, the corporate maintains an affordable payout ratio of 63.6%, making certain that dividends are adequately lined by earnings. Moreover, with a money payout ratio of 85.7%, its dividend funds are additionally supported by money flows. Nevertheless, latest monetary outcomes present a decline in web earnings and primary earnings per share year-over-year as of Q1 2024, coupled with decrease revenue margins in comparison with the earlier yr, which may increase considerations about future dividend reliability and development prospects.

Seize The Alternative

In Different Prospects?

This text by Merely Wall St is basic in nature. We offer commentary based mostly on historic knowledge and analyst forecasts solely utilizing an unbiased methodology and our articles should not meant to be monetary recommendation. It doesn’t represent a suggestion to purchase or promote any inventory, and doesn’t take account of your goals, or your monetary state of affairs. We purpose to carry you long-term targeted evaluation pushed by basic knowledge. Notice that our evaluation could not issue within the newest price-sensitive firm bulletins or qualitative materials. Merely Wall St has no place in any shares talked about.

Corporations mentioned on this article embody KOSDAQ:A011560 KOSDAQ:A036190 and KOSE:A004000.

Have suggestions on this text? Involved in regards to the content material? Get in contact with us immediately. Alternatively, e mail editorial-team@simplywallst.com