It’s a lonely occupation betting in opposition to semiconductor juggernaut Nvidia (NASDAQ:NVDA), which is why nobody does it. Probably the most you’re going to seek out amongst Wall Road specialists are a uncommon handful of Maintain scores. Nevertheless, as a result of seemingly everyone seems to be amped up concerning the firm’s upcoming earnings report, comparatively few recognize the dangers tied to making an attempt to hit ever-rising monetary targets. Given the info, I’m near-term bearish on NVDA inventory.

Even NVDA Inventory Wants a Breather

Essentially, the core concern surrounding NVDA inventory facilities on the underlying firm’s potential to maintain impressing. For instance, a sofa potato decided to make good on a brand new 12 months’s well being and health decision can take pleasure in important beneficial properties by means of comparatively minor effort exerted. Nevertheless, observe famous person Usain Bolt in his prime would solely accrue incremental efficiency returns, if something.

Clearly, one is ranging from a low base and, due to this fact, advantages from the presence of low-hanging fruit. Within the case of Bolt and NVDA inventory, these elite gamers solely face high-hanging fruit. Additional, with Nvidia persevering with to impress onlookers with its blistering monetary performances, the expectations proceed to speed up. In some unspecified time in the future, the fruit will likely be hanging so excessive that it’s going to require using a crane to succeed in it.

On the anticipated date of February 21, Nvidia will disclose its outcomes for the fourth quarter of Fiscal 2024. Analysts name for the corporate to ship earnings per share of $4.59, effectively above the 81 cents it posted in This fall of the prior 12 months. In Q3, Nvidia posted EPS of $4.02 in opposition to the consensus of $3.37. Subsequently, one other beat isn’t out of the query.

Moreover, these bullish on NVDA inventory will level to Nvidia’s dominance in AI-centric graphics processing models (GPUs). As effectively, booming demand within the information heart ecosystem might assist undergird Nvidia’s prime and backside traces. Lastly, a number of business analysts have talked a couple of second wave in AI that will facilitate unbelievable developments in machine studying and neural networks.

You’ll discover few who disagree with the elemental catalysts augmenting NVDA inventory. Nevertheless, these are additionally recognized catalysts which have possible been priced in.

Too A lot Bullishness Baked Into the Nvidia Commerce

Essentially, one of many greatest points with NVDA inventory is that primarily based on transactions recorded within the uncommon choices exercise screener – the sector the place the sensible cash is arguably most lively – not a lot incentive exists for bearish merchants when buying and selling for intrinsic worth (versus playing on extrinsic worth appreciation).

For instance, for choices seeing uncommon exercise that expire on June 21, 2024, the most cost effective name primarily based on whole value (that’s, the price to train added to the whole contract premium) is the $675 name, with an outlay of $79,220. Whereas steep, primarily based on a linear trajectory of probably the most optimistic worth goal, by the June 21 expiration, NVDA inventory could also be price $884.09 per share.

Multiply the aforementioned determine by 100 shares, and the worth comes out to $88,409. Nevertheless, you’d be worthwhile as a result of the price to amass this place was $79,220.

Now, contemplate the put aspect of the argument. The most cost effective June 21 put, which might actually have a likelihood of being worthwhile (that’s, the strike worth is larger than the market worth), is the $675 put. Primarily based on probably the most pessimistic worth goal, NVDA inventory might drop to $670.75 by the expiration date. On the gross degree, you’d have a contract that permits you to promote NVDA at $675 versus practically $671.

Nevertheless, the premium for this put stands at $52.40. Multiply that by 100 shares added to the price of exercising, and abruptly, it makes zero sense to purchase this put in the event you’re going strictly for intrinsic worth.

What’s extra, searching to the February 21, 2025 expiration date, the most cost effective name by way of whole contract worth is the $700 strike. Right here, buyers can count on to pay $86,880 (contract premium of $168.8 multiplied by 100 shares plus the exercising of 100 shares at $700). Nevertheless, if NVDA inventory can attain the very best analyst goal of $1,200, the place would yield a revenue of $33,120.

On the flip aspect, the most cost effective put for the February 21 expiration date is the $730 put. Right here, buyers should pay a complete value of $84,600 (contract premium of $116 multiplied by 100 shares plus the exercising of 100 shares at $730). Ought to NVDA inventory fall to the bottom worth goal of $560, the place would revenue solely $5,400.

In fact, one may all the time purchase, say, the $600 January 2025 put and speculate on the worth of the contract growing forward of schedule. Nevertheless, such a wager represents a deeper danger that the choice won’t be salvageable and even near being salvageable. In distinction, the decision aspect options many avenues for hypothesis at extra comparatively enticing charges.

In the end, this framework incentivizes merchants to go lengthy, which appears aggressive. Sure, Nvidia is a real juggernaut, however no firm rises larger indefinitely.

A Main Warning Issued

One other ingredient that makes me jittery concerning the extreme bullishness in NVDA inventory stems from a significant warning signal that hit final Friday. Shares of Tremendous Micro Laptop (NASDAQ:SMCI) tumbled 20% following a stratospheric run because the starting of this 12 months. Even with the fallout in SMCI, it’s nonetheless up over 182% year-to-date.

However, that’s a deafening shot throughout the bow relating to the rabid AI-driven enthusiasm for the corporate. Sure, the corporate’s server and storage options supply important implications for digital intelligence. Nevertheless, some analysts have argued that this narrative is already priced in.

Frankly, the identical might be stated about NVDA inventory. Once more, nobody doubts that Nvidia will play a dominant position within the processes of the longer term. Nevertheless, sentiment is just too far stacked on one aspect of the commerce.

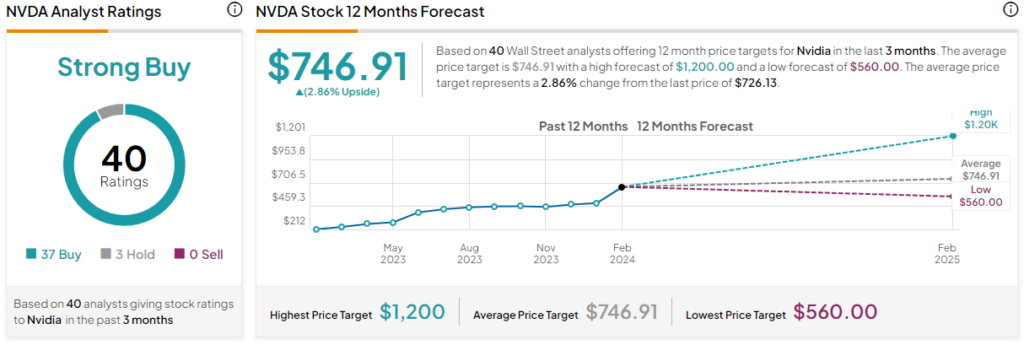

Is NVDA Inventory a Purchase, In response to Analysts?

Turning to Wall Road, NVDA inventory has a Robust Purchase consensus ranking primarily based on 37 Buys, three Holds, and 0 Promote scores. The common NVDA inventory worth goal is $746.91, implying 2.86% upside potential.

The Takeaway: Even NVDA Inventory Will Want a Breather Quickly

It may well’t be careworn sufficient: Nvidia is an incredible enterprise with a profoundly encouraging future forward of it. With its dominance in GPUs that may assist energy the most recent AI-based improvements, it’s well-positioned for the long term. Nevertheless, information from the choices market means that sentiment is excessively stacked in favor of the bulls. Given the more and more rising expectations, buyers must be cautious about NVDA inventory within the close to time period.

Disclosure

{kind=link}